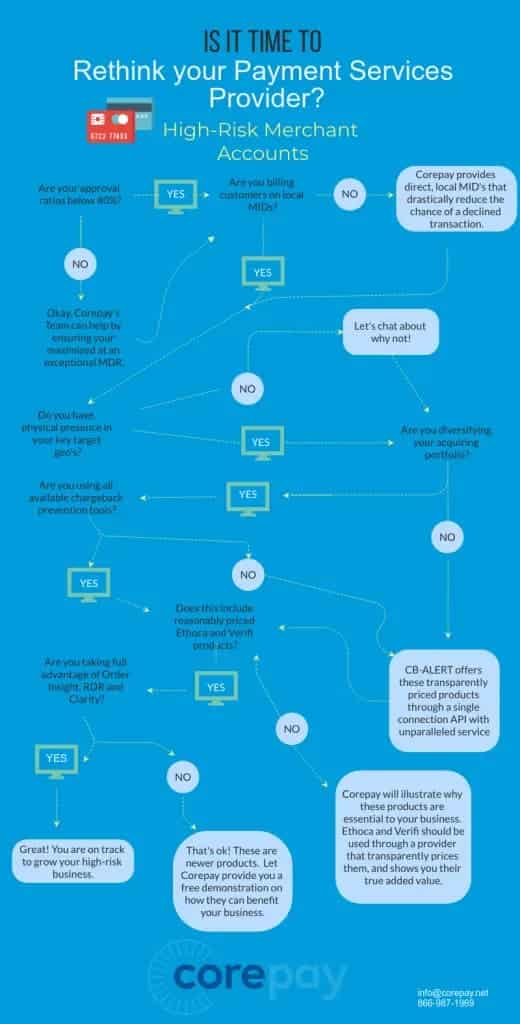

High Risk Merchant Accounts

Approved Where Other Processors Decline

Dedicated merchant accounts for specialty businesses with fast approvals, transparent pricing, and no industry restrictions.

Fast Approvals

Most specialty accounts are approved within one to three business days.

Chargeback Protection

Built-in fraud tools and dispute management keep your account in good standing.

Global Coverage

Accept payments across the US, UK, EU, and Canada with a single merchant account.

See How Your Rates Stack Up

High risk merchants often overpay because they have fewer options. Enter your volume and current rate to see what we can offer.

- We approve industries others decline

- Interchange-plus pricing, no hidden markups

- No application or setup fees

How much are you overpaying?

Enter your numbers from last month's processing statement.

All figures shown are estimates only and may be subject to change based on application review, business model, risk factors, and underwriting assessments. This tool does not constitute a commitment, guarantee, or offer of specific terms.

Same-day decisions · No application fee · Dedicated account manager

High Risk Accounts Built Around Your Business

What Sets Our High Risk Accounts Apart

Specialty Underwriting

Standard processors approve accounts quickly and terminate them just as fast when the industry type is flagged. We underwrite every application in full before approval. That means no surprises after go-live: no sudden holds, no fund freezes, no terminations when your volume grows.

Transparent Pricing

Interchange Plus pricing with no hidden markups. Your statement shows exactly what you paid and why, every billing cycle.

No Setup Fees

No application fees, no setup fees, no annual fees. You pay for processing activity, nothing else.

Rolling Reserve Options

We structure reserves fairly and release them on a predictable schedule as your account matures and chargeback rate stabilizes.

Dedicated Account Manager

One contact from application through your first year. They know your account, your industry, and your processing history.

Industry Coverage

We approve merchant accounts across a wide range of specialty verticals: healthcare, telehealth, online pharmacy, medspa, CBD, subscription billing, and others that standard processors decline by default. Your industry is not the deciding factor. Your processing history, chargeback rate, and business model are.

Processing Payments in 30+ Countries

United States

50 statesFull domestic processing with next-day funding and dedicated account management.

European Union

27 member statesPSD2 and SCA compliant processing across all EU member states with multi-currency settlement.

United Kingdom

England, Scotland, Wales, NIFCA-regulated payment processing with GBP settlement and local acquiring.

Australia

All territoriesAPRA-compliant processing with AUD settlement and Asia-Pacific connectivity.

Works With Your Existing Stack

Your high risk merchant account connects to the platforms you already run, from Shopify to custom APIs.

Browse all integrations

What Is a Specialty Merchant Account?

A specialty merchant account is a payment processing account for businesses that fall outside what standard processors are willing to approve. Standard processors use broad industry codes to automate underwriting decisions. If your category is flagged, the account is declined or terminated, often without explanation.

Specialty accounts are underwritten individually. The processor reviews your actual business: your chargeback history, your refund policy, your sales model, and your compliance posture. The result is an account that fits your business instead of one that barely tolerates it.

Why Standard Processors Decline Specialty Businesses

Payment aggregators and general-purpose processors manage risk through volume. They approve thousands of accounts automatically and close the ones that cause problems later. For specialty merchants, this model creates serious operational risk.

The most common reasons for decline or termination include:

- Industry category associated with elevated chargeback rates

- Subscription billing or free trial models that generate disputes

- Products or services that card networks restrict or monitor closely

- Prior account termination or placement on the MATCH list

- Processing volume or transaction size outside the aggregator model

None of these factors automatically disqualify a business from accepting payments. They require a processor who is equipped to underwrite them properly.

Industries We Approve

We work with businesses across a broad range of specialty verticals, including:

- Nutraceuticals and dietary supplements

- iGaming and online gaming operators

- Subscription billing and membership businesses

- Travel agencies and tour operators

- Telemedicine and online pharmacies

- Age-verified content platforms

- Hemp and CBD products

- Med spas and wellness clinics

If your industry is not listed, contact us. Our underwriting team reviews each application individually and can advise on eligibility before you submit.

How Our Underwriting Process Works

Our underwriting team reviews every application before approval. We look at the full picture of your business rather than applying a blanket policy based on industry type.

The key factors we evaluate include:

- Chargeback and refund history across prior processing accounts

- Business registration, licensing, and compliance documentation

- Bank statements and financial history

- Website compliance: terms of service, refund policy, contact information

- Processing volume and average transaction size

Upfront underwriting protects both sides. You know your account is stable before you go live. We know the account is structured correctly for the risk profile.

What to Prepare for Your Application

To move through underwriting quickly, have the following ready when you apply:

- Business bank statements, three months minimum

- Government-issued ID for all principals with 25% or more ownership

- Business registration documents and EIN

- Three to six months of processing statements, if available

- Any licensing documentation relevant to your industry

- A compliant website with terms of service and a refund policy

Once approved, your dedicated account manager will walk you through reserve terms, gateway setup, and any compliance requirements specific to your vertical.