CBD Payment Processing

CBD Merchant Accounts Built to Last

Stable, long-term CBD merchant accounts backed by dedicated banking relationships and in-house underwriters.

Fast Approvals

Most CBD merchants receive a decision within 24 hours of submitting a complete application.

Chargeback Protection

Our in-house fraud tools and real-time dispute alerts keep your chargeback ratio well below card network thresholds.

Seamless Gateway Integration

Connect Shopify, WooCommerce, or any custom store to our proprietary CBD-ready payment gateway.

See How Your CBD Processing Rates Compare

CBD merchants pay higher rates due to limited banking options. Enter your volume to see what we can offer.

- Dedicated CBD banking relationships

- LegitScript certification support

- Streamlined onboarding for most CBD merchants

How much are you overpaying?

Enter your numbers from last month's processing statement.

All figures shown are estimates only and may be subject to change based on application review, business model, risk factors, and underwriting assessments. This tool does not constitute a commitment, guarantee, or offer of specific terms.

Same-day decisions · No application fee · Dedicated account manager

Why CBD Merchants Choose Corepay

Most banks refuse CBD merchants outright. We maintain dedicated CBD banking relationships and offer a streamlined approval process.

Challenges CBD Merchants Face

Account Terminations Without Notice

Standard processors regularly shut down CBD accounts without warning, leaving merchants unable to accept payments overnight.

Limited Banking Options

Most acquiring banks refuse CBD entirely, making it nearly impossible to find a reliable long-term payment partner.

Chargeback Accumulation

Without proper fraud tooling, CBD merchants often see chargeback ratios that jeopardize accounts and trigger card network reviews.

Regulatory Uncertainty

Shifting federal and state regulations make it difficult to find a processor willing to commit to a stable, long-term banking relationship.

Built for CBD Commerce

Dedicated CBD Banking

We maintain direct banking relationships specifically for CBD merchants, with no shared accounts and no surprises.

Fast Decisions

Our in-house underwriting team reviews CBD applications fast, with most decisions coming back within 24 hours.

Proprietary Gateway

Our payment gateway supports all major card brands, recurring billing, and advanced fraud controls built specifically for CBD.

LegitScript Support

We work closely with LegitScript to help CBD merchants meet certification requirements and maintain their accounts in good standing.

Chargeback Alert System

Real-time Ethoca and Verifi alerts notify you of disputes before they become chargebacks, giving you time to resolve them directly.

Dedicated Account Manager

A named account manager with CBD industry experience handles your account from day one, available around the clock.

Corepay By the Numbers

-

Fast Approval Turnaround

-

20+ Years Specialty Experience

-

135+ Currencies Supported

How CBD Merchant Approval Works

Submit Your Application

Complete our 5-minute online application with your business details, website URL, and current processing volume.

Underwriting Review

Our CBD specialists review your application and supporting documents, with most decisions delivered within 24 hours.

Account Configuration

We configure your gateway, connect your storefront, and set up fraud rules tuned to your CBD business.

Start Processing

Your account goes live and you begin accepting payments, with dedicated support available around the clock.

Processing Payments in 30+ Countries

United States

50 statesFull domestic processing with next-day funding and dedicated account management.

European Union

27 member statesPSD2 and SCA compliant processing across all EU member states with multi-currency settlement.

United Kingdom

England, Scotland, Wales, NIFCA-regulated payment processing with GBP settlement and local acquiring.

Australia

All territoriesAPRA-compliant processing with AUD settlement and Asia-Pacific connectivity.

Selling CBD should not feel harder than formulating it. If you are in this space, you already know the problem is not demand. It is banking. Accounts get frozen. Applications get declined. Aggregators approve you on Monday and shut you down on Friday. And suddenly your revenue is on hold while your inventory keeps moving.

CBD is still treated as high-risk by most banks and payment facilitators. Between evolving regulations, card network scrutiny, and compliance requirements, many traditional processors simply do not want the exposure. That leaves serious CBD brands stuck cycling through unstable providers.

We specialize in high-risk merchant accounts, including CBD, hemp-derived products, and compliant ingestibles. With decades of experience underwriting complex industries, we know exactly how to structure your application, position your business correctly, and secure stable acquiring relationships that are designed to last.

Our goal is simple: get you approved and keep you processing without disruption.

How to Apply

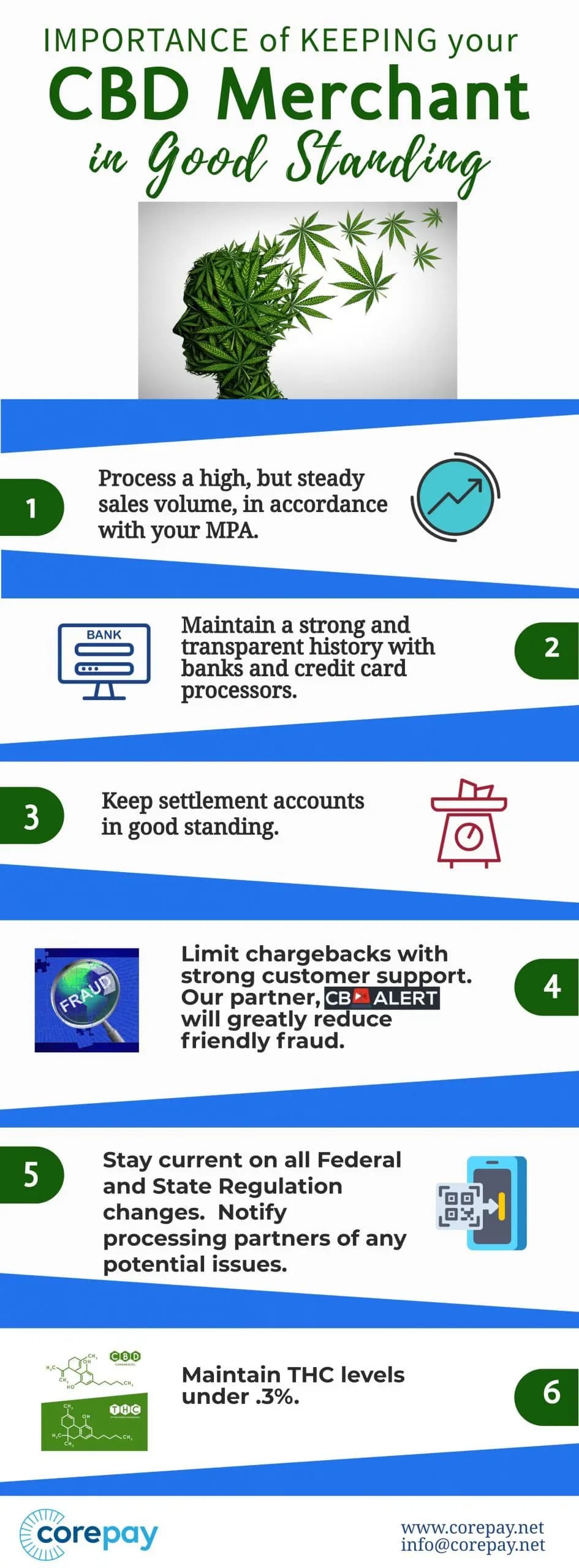

CBD merchants selling hemp-derived products with THC levels of 0.3 percent or below can apply for a merchant account. We cannot provide accounts for any cannabis products containing THC above 0.3 percent.

You will need the following information when applying:

- A voided check

- A valid government I.D. (driver’s license)

- Six months of processing statements showing chargeback performance

- Articles of Incorporation

- SSN

- Fulfillment agreement

- A secure, fully compliant website

What We Offer CBD Merchants

As the CBD industry expands and encompasses new products, we work to maintain reliable service for every merchant on our platform.

- Fast approvals within 24 to 72 hours

- No application, annual, or setup fees

- Risk mitigation through Order Insight by Verifi

- Chargeback alerts

- Rates as low as a blended 2.95%

FDA Regulations and CBD Processing

The lack of broad FDA approval is a major concern for payment providers serving the CBD space. The only FDA-approved drug containing CBD is Epidiolex, a purified formulation used to treat seizures. The FDA has taken action against several CBD companies for making unsupported claims about medical benefits.

Because THC levels in CBD products can vary, processors face real compliance risk. If a CBD company is found selling products with THC above 0.3 percent, the payment provider can face financial and reputational consequences. This is why most traditional processors avoid the category entirely.

CBD Chargebacks

Chargebacks in the CBD industry tend to be lower than in other high-risk verticals like online dating or adult content. That said, they still occur, especially with online CBD stores and subscription models.

A chargeback is a charge returned to a credit card after a customer successfully disputes a transaction. In the CBD space, this is most common with subscription boxes, where recurring billing can lead to disputes from customers who forget they signed up or have trouble cancelling.

Here are a few things to keep in mind when choosing your merchant service provider:

- Pricing: specialty merchant accounts typically carry higher fees than standard accounts. We offer interchange-plus pricing as well as traditional merchant discount rates. Expect a rolling reserve, a portion of each settlement held temporarily to protect against chargebacks and fraud.

- Account approval: be cautious of providers that approve you instantly. That usually means your account was opened without a proper underwriting review, which can lead to problems later.

- Hardware: if you sell both online and in-store, you will need a credit card terminal or mobile processing system capable of accepting EMV and contactless payments.

- Contracts: CBD merchant account contracts vary between providers. Some require early termination fees, but this is often negotiable.

- Support: ecommerce support is critical for CBD processing. We can help you configure your gateway to restrict orders from zip codes where CBD is not permitted by law.

Is CBD Credit Card Processing Expensive?

CBD merchants will generally pay more for processing than standard merchants, because the category is classified as high-risk. That said, we offer competitive rates and waive application fees, annual fees, and setup fees. We believe a good processor earns your loyalty through transparent pricing, not hidden charges.

Why Choose Corepay

We specialize in the CBD industry and in high-risk merchant accounts broadly. We understand what it takes to get merchants approved and keep them growing. We offer fully customizable credit card processing and can get you approved in as little as 24 hours after you submit your application.