Visa Rapid Dispute Resolution

Auto-Resolve Disputes Before Chargebacks Post

Visa's Rapid Dispute Resolution lets you set rules that automatically refund eligible disputes before they become chargebacks, reducing your ratio without manual intervention.

Rule-Based Automation

Set criteria for which disputes to automatically accept and refund. Matching disputes are resolved instantly, before a chargeback ever reaches your account.

Chargeback Ratio Protection

By resolving disputes before they post, RDR keeps your ratio well below the thresholds that trigger card network monitoring programs.

No Manual Review Required

Once your rules are configured, RDR handles matching disputes automatically. Your team only gets involved when a dispute falls outside your ruleset.

See What Auto-Resolution Can Save You

Every chargeback that RDR resolves automatically saves you the dispute amount plus fees. Enter your Visa dispute volume to see the impact.

- Disputes resolved before they post as chargebacks

- Custom rules by amount, reason code, and issuer

- Pairs with Verifi alerts and Ethoca for full coverage

How much are you overpaying?

Enter your numbers from last month's processing statement.

All figures shown are estimates only and may be subject to change based on application review, business model, risk factors, and underwriting assessments. This tool does not constitute a commitment, guarantee, or offer of specific terms.

Same-day decisions · No application fee · Dedicated account manager

Set Your Rules, Let RDR Handle the Rest

When a Visa dispute matches your criteria, RDR automatically issues a refund and stops the chargeback before it posts. You control which disputes are auto-resolved and which require your review.

Smart Automation for Dispute Resolution

Fully Automated Dispute Resolution

RDR evaluates every incoming Visa dispute against your ruleset the moment it arrives. Disputes matching your criteria are auto-resolved and the cardholder refunded immediately, stopping the chargeback before it posts. No manual review, no delay, no chargeback fee on resolved disputes.

Custom Resolution Rules

Define rules by transaction amount, dispute reason code, product type, currency, or issuer. RDR only auto-resolves disputes that meet your parameters.

Chargeback Ratio Control

By resolving eligible disputes proactively, RDR keeps your chargeback ratio below Visa's threshold and out of monitoring programs.

Dispute Analytics and Reporting

Track which disputes RDR resolves, which fall outside your rules, and where your chargeback exposure concentrates. Use the data to refine your ruleset over time.

Works with Order Insight

RDR pairs with Visa's Order Insight tool, which provides dispute context to issuers before they escalate. Together they reduce disputes at multiple stages.

Part of Your Full Dispute Stack

RDR handles automated Visa resolution while Verifi alerts give you manual review time and Ethoca covers Mastercard. We enroll you in all three and manage them as a unified service, so every dispute is handled the right way.

Processing Payments in 30+ Countries

United States

50 statesFull domestic processing with next-day funding and dedicated account management.

European Union

27 member statesPSD2 and SCA compliant processing across all EU member states with multi-currency settlement.

United Kingdom

England, Scotland, Wales, NIFCA-regulated payment processing with GBP settlement and local acquiring.

Australia

All territoriesAPRA-compliant processing with AUD settlement and Asia-Pacific connectivity.

Connects to Your Gateway and CRM

RDR integrates with your payment gateway and order management system so that auto-resolved disputes trigger downstream actions like subscription cancellations and shipment holds.

Browse all integrations

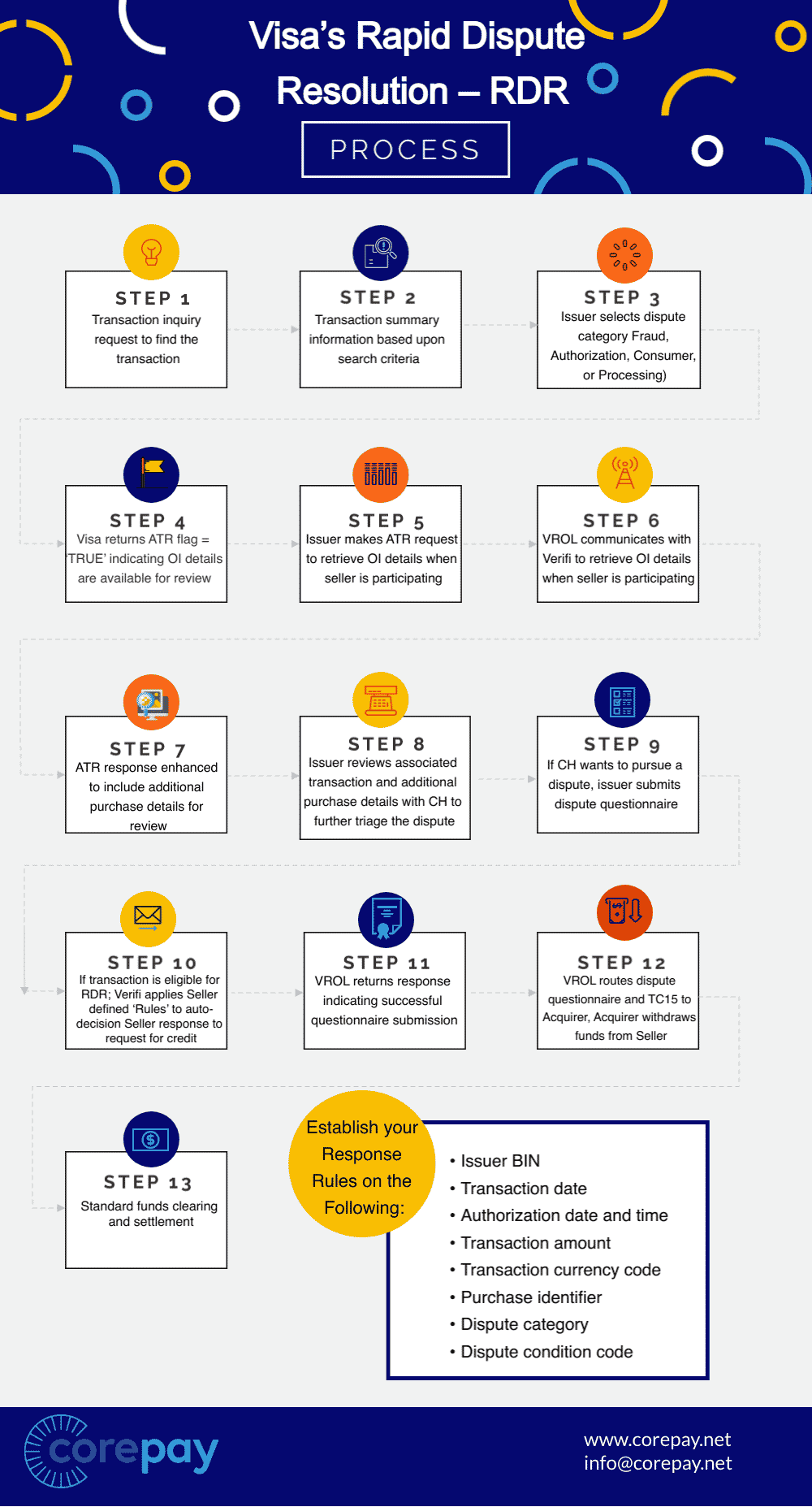

How Visa RDR Works

Visa’s Rapid Dispute Resolution is an automated system built on the Verifi platform. When a Visa cardholder initiates a dispute, the system checks the dispute against your pre-configured ruleset before the chargeback is filed. If the dispute matches your criteria, RDR automatically issues a refund and closes the dispute. The chargeback never posts to your account.

Disputes that do not match your ruleset are handled differently depending on your setup. They can be paused and forwarded to you as a Verifi alert for manual review, or allowed to proceed through the standard chargeback process. This gives you full control over which disputes are auto-resolved and which require your judgment.

Configuring Your RDR Ruleset

The effectiveness of RDR depends on how well your rules match your actual dispute patterns. Rules can be based on transaction amount, dispute reason code, product category, currency, purchase date, issuer bank ID, and other variables. We configure your initial ruleset based on your transaction profile and chargeback history, then monitor results and recommend adjustments over time.

A common starting strategy is to auto-resolve all disputes below a threshold amount (for example, transactions under $75) regardless of reason code, since the cost of reviewing and potentially winning those disputes often exceeds the refund value. From there, you can layer in more specific rules based on product type or dispute category.

RDR, Verifi Alerts, and Order Insight Together

Visa offers three related tools that address disputes at different stages of the lifecycle. Order Insight is the first line of defense: it provides dispute context to issuers before a cardholder formally files, resolving many disputes before they reach the alert stage. Verifi alerts are the second layer: manual notifications for disputes that require your review. RDR is the third layer: automated resolution for disputes that match your rules.

Using all three tools together maximizes your dispute prevention rate at every stage. We enroll you in whichever combination fits your transaction volume and dispute profile.

Who Benefits Most from RDR?

RDR delivers the highest return for merchants with high Visa transaction volume who cannot manually review every incoming dispute. Subscription billing merchants, nutraceutical brands, digital content businesses, and iGaming operators all see significant value from automated dispute resolution.

For merchants approaching Visa’s VAMP merchant standard of 1.50%, RDR is often the fastest way to bring the ratio down. By resolving eligible disputes before they post, you can significantly reduce your chargeback count without increasing your refund rate, since RDR disputes would have converted to chargebacks anyway.