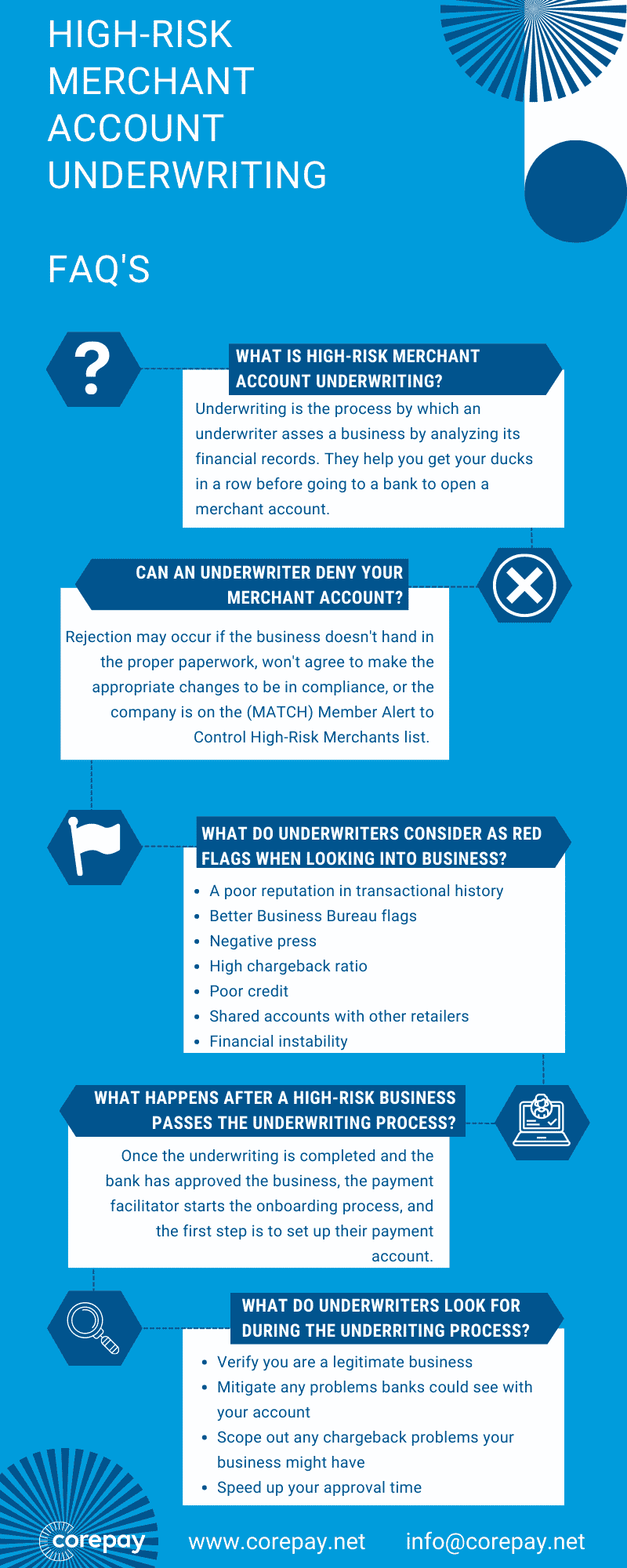

High Risk Underwriting

Approvals Built Around Your Full Story

We review your application holistically before it reaches the bank, addressing potential concerns upfront so your account gets approved faster.

Pre-Bank Review

We underwrite your account before submitting to the acquiring bank, identifying and addressing issues that could slow or stop approval.

Fast Decisions

Our pre-approval process is streamlined so most merchants get a decision within one business day of submitting a complete application.

Dedicated Application Support

A dedicated account manager guides you through the application, helps you prepare documents, and communicates with the bank on your behalf.

See How Fast You Can Get Approved

Most high risk merchants wait weeks for a decision. We pre-review your application and return a decision within one business day.

- Fast pre-approval for complete applications

- We resolve concerns before the bank sees your file

- One point of contact from application to approval

How much are you overpaying?

Enter your numbers from last month's processing statement.

All figures shown are estimates only and may be subject to change based on application review, business model, risk factors, and underwriting assessments. This tool does not constitute a commitment, guarantee, or offer of specific terms.

Same-day decisions · No application fee · Dedicated account manager

Your Full History, Reviewed Before Submission

Underwriting Done Right, from the Start

Holistic Account Review

We evaluate your complete business picture: processing history, chargeback ratios, financial statements, business documentation, and website compliance. This pre-submission review lets us resolve concerns before they reach the acquiring bank, dramatically improving your approval odds and reducing back-and-forth delays.

Fast Decisions

Most merchants with complete applications receive a pre-approval decision within one business day. No waiting weeks for a bank response.

Chargeback History Analysis

We review your chargeback ratios and flag any patterns that could concern an acquiring bank, with recommendations to address them before submission.

Document Preparation Guidance

We tell you exactly what documents you need and review them before submission so nothing is missing when it counts.

Bank Communication on Your Behalf

Once submitted, we stay engaged with the acquiring bank throughout the review. You have one point of contact: us.

Path to Better Terms Over Time

Strong underwriting at the start of your relationship is how merchants earn lower reserves and better rates over time. We document your performance and advocate for improved terms as your processing history builds.

Processing Payments in 30+ Countries

United States

50 statesFull domestic processing with next-day funding and dedicated account management.

European Union

27 member statesPSD2 and SCA compliant processing across all EU member states with multi-currency settlement.

United Kingdom

England, Scotland, Wales, NIFCA-regulated payment processing with GBP settlement and local acquiring.

Australia

All territoriesAPRA-compliant processing with AUD settlement and Asia-Pacific connectivity.

Ready to Integrate on Day One

Once approved, your merchant account connects immediately to your payment gateway, shopping cart, and CRM. No waiting period, no separate integration process.

Browse all integrations

What Specialty Merchant Underwriting Covers

Merchant account underwriting is more thorough for specialty merchants than for standard businesses. Because acquiring banks take on additional risk when processing payments for complex industries, they review your application more carefully before extending a merchant account relationship.

The underwriting review typically covers: your business structure and legal documentation, your processing history and chargeback ratios, your financial statements and business bank account, your website and marketing practices, and any prior merchant account terminations or disputes. Each of these areas gives the acquirer a clearer picture of the risk profile they are taking on.

How Our Pre-Submission Review Works

Most payment processors submit your application directly to an acquiring bank and wait for a response. We take a different approach. Before your application goes anywhere, our underwriting team reviews it first.

We verify that your documentation is complete, check your chargeback history against acquiring bank thresholds, review your website for compliance requirements, and identify any factors that could complicate approval. If we find concerns, we work with you to address them before submission. This pre-review process is why our approval timelines are faster and our approval rates are higher than going directly to a bank.

What Strengthens a Specialty Merchant Application

The strongest applications share a few common characteristics. A low chargeback ratio (below one percent) is the single most important factor. Banks want to see that your business has a history of clean processing, or that you have a credible plan to keep disputes low.

Consistent processing history also helps, even if volume is modest. Six months of stable processing with the same processor is generally more valuable than a short period of high volume. If you are a new business without processing history, strong bank statements and a clearly documented business model can compensate.

Good business credit, a professional website with clear terms and refund policies, and responsive communication during the application process all contribute to a stronger outcome. Businesses that are hard to reach or vague about their operations tend to face more scrutiny during underwriting.

What to Expect at Each Stage

Once you submit your application, we begin our pre-review immediately. If everything is in order, you receive a pre-approval decision from us within one business day. We then submit to the acquiring bank, where the formal underwriting review takes place. This stage typically adds three to five business days depending on the bank and your industry category.

Throughout the process, you communicate with us, not directly with the bank. We handle questions, gather any additional documentation the bank requests, and advocate for your account through the review. Once approved, your account is set up and ready to integrate with your payment stack immediately.