ACH VS E-Checks – What To Use

ACH vs e-checks explained. How each payment method works, key differences in processing and timing, and which is better for your business.

Automated Clearing Houses (ACH) and e-checks are two prevalent transactions when transferring between bank to bank.

Consumers, small business owners, and even larger companies send or receive payments as e-checks/ACH. Unfortunately, these terms are often thrown around by those unfamiliar as interchangeable.

While they are similar, there are some critical differences between ACH and e-checks. As transaction volumes and the frequency increase with ACH and e-checks, it becomes essential that business owners learn the differences between the two.

If you’re a business owner looking to find the key differences between ACH and e-checks and which is better for your business, you’veyou’ve come to the right place.

Over the last few years, it has become even more critical as more businesses accept and send payment via ACH and e-check.

Side note: We also recommend checking out our article on ACH Vs. Wire transfers if you want to learn more about transferring funds.

E-Checks Vs. ACH

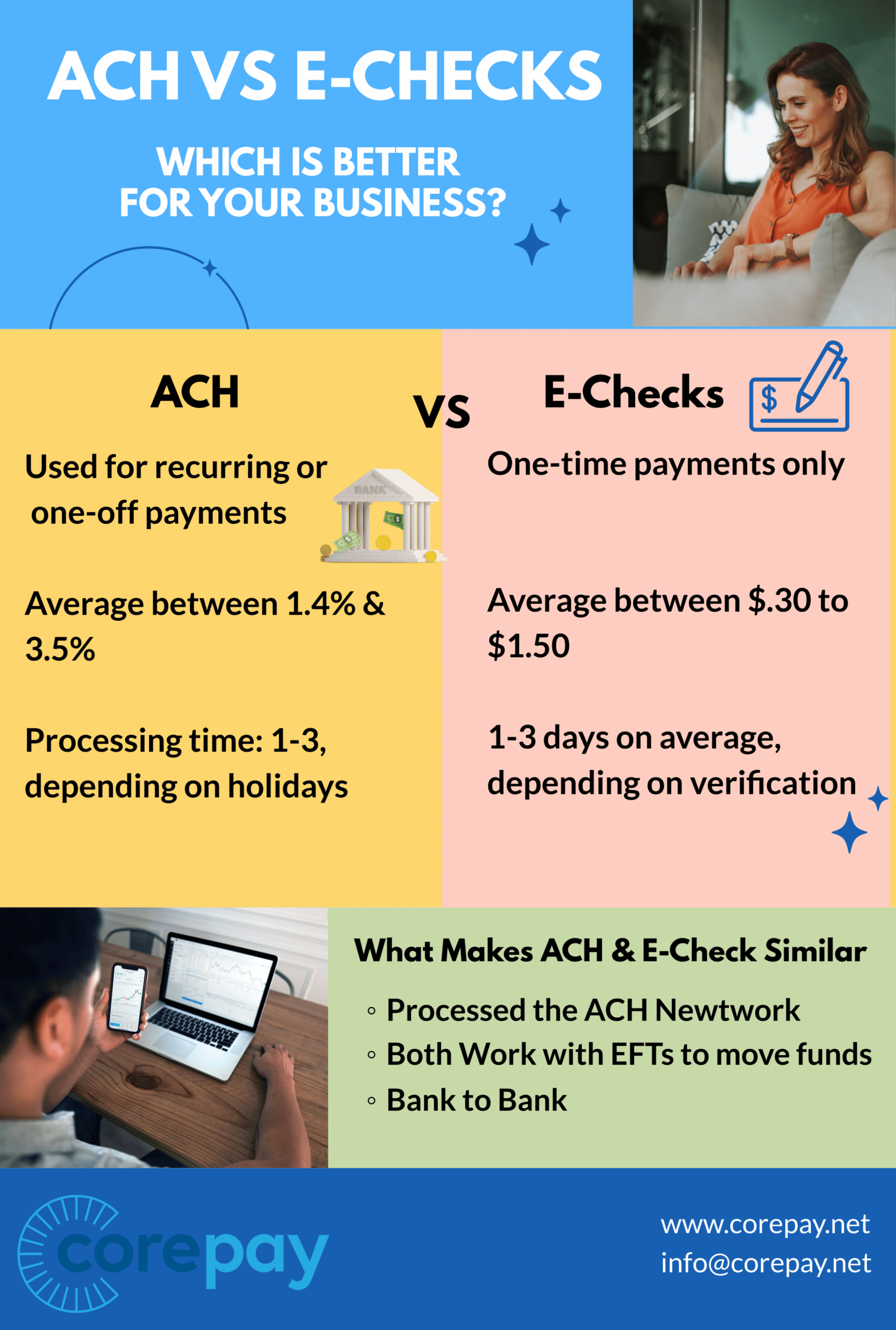

Before we break down e-checks and ACH, let’s get right to it and explain the main differences. For a simple answer: If you are doing a one-off payment, e-Checks are great. If you are looking for recurring payments, ACH is the way to go.

Frequency

Frequency is an area that these two methods can differ:

ACH: Can be one-offs and can also be recurring

E-Checks: One-time payments

Cost:

ACH: Between 1.4% and 3.5% on average

E-Checks: On average, $.30 to $1.50

Processing Time

ACH: 1-3 days depending on holidays

E-Checks: 1-3 days on average. It can take longer, depending on how long it takes to verify the transaction.

What Is An ACH Payment?

An ACH payment is a type of electronic bank-to-bank payment that uses the Automated Clearing House System instead of going through card networks, wire transfers, cash, or checks.

The Automated Clearing House network is a network established for electronic financial transactions in the United States. The network allows financial institutions to communicate efficiently regarding transactions associated with accounts held by the banks. In addition, the network is designed so that large numbers of payments can be made at once.

What Is An E-Check?

E-checks are precisely what you would expect, a digital check.

Check payments are made through the Automated Clearing House (ACH) Network, which transfers funds between bank accounts. Unlike a traditional paper check that is processed manually, eChecks are processed electronically. To process the Echeck, you must work with a payment processor that accepts e-checks.

Difference Between E-Checks and ACH And Why Each Are Used

Although we have highlighted the core differences, let’s briefly break down what happens once an e-check or ACH payment is submitted.

Once the payer submits an eCheck which includes the following:

- Details of checking/banking account

- routing number

- bank account number

- authorization to process the E-check

The payee or the merchant will receive it; thus, the payment gets processed through the ACH network.

Regarding an ACH payment, the transfer is made using bank routing numbers and bank account information. This entire process takes 1-3 days, on average, holiday depending. While this takes longer than a wire transfer or a debit card, the cost is significantly lower.

An example of when a business should implement ACH payments is if the payment is recurring to a freelancer. For example, say a company outsources to the same freelancer for web development that is recurring monthly; this is a great time to take advantage of ACH.

Processing Fees For ACH And E-Checks

When authorized, ACH processing and e-check processing take the same time. You can expect 1-3 business days; however, e-checks have an additional step that can make them take longer than ACH payments.

Since E-checks are one-time payments, the merchant account needs verification before it can process the e-check through the ACH network. This process can sometimes add on between 12-48 hours.

Implementation Of ACH And E-CHecks

Both ACH payments and eChecks are essential to accept and receive for all business owners. When you break it down, processing fees are relatively low, customers appreciate the convenience, and they are secure.

Since transfers come straight from customers’ accounts, they can avoid fees, likewise for merchants.

If you have the right payment processing partner, these solutions are simple.

What Makes ACH And E-Checks Similar?

Since we have already gone over the differences between ACH payments and e-checks, you can easily assume the similarities.

The following is true of both ACH and e-checks:

- Processed the ACH network

- Both work with EFTs (electronic fund transfers) to move funds

- Bank to bank

Why Choose Corepay

At Corepay, we prioritize our clients and make sure they are on the right track in all things payment processing.

We can handle your ACH needs at minimum pricing and help with your everyday needs with payment processing.

We can offer:

- Waived fees (application, set up, annual)

- Risk mitigation with Rapid Dispute Resolution (RDR) by Verifi, 3-D Secure 2.1/ our partner product CB-ALERT

- Traditional chargeback alerts by Ethoca and Verifi

- Rates as low as a blended 2.95%

- Maximize approval ratios due to routing technology based on your target customer base within our proprietary payment gateway

Wrapping Up

E-checks and ACH both have their place when it comes to the transferring of funds. If you are confused about which practice is best for your business, feel free to reach out at the link below.

Contact Us/Apply