Debt Collection Payment Processing

Merchant Accounts for Debt Collection Agencies

Reliable payment processing for debt collection agencies and accounts receivable management companies.

FDCPA-Aware Underwriting

Our underwriting team understands the Fair Debt Collection Practices Act and works with licensed collection operations.

Fast Approvals

Most debt collection merchants receive a decision within 24 to 72 hours of submitting a complete application.

ACH & Card Processing

Accept payments by credit card, debit card, and ACH to maximize recovery rates from debtors.

See How Your Collection Rates Compare

Collection agencies pay premium rates because most processors ban the category. Enter your volume to see what we can offer.

- ACH and card payment acceptance

- FDCPA-aware underwriting

- Chargeback alerts for disputed debts

How much are you overpaying?

Enter your numbers from last month's processing statement.

All figures shown are estimates only and may be subject to change based on application review, business model, risk factors, and underwriting assessments. This tool does not constitute a commitment, guarantee, or offer of specific terms.

Same-day decisions · No application fee · Dedicated account manager

Processing Built for Collection Agencies

Challenges Collection Agencies Face

Chargeback Risk From Disputed Debts

Debtors who dispute the underlying obligation frequently file chargebacks after making payments. Without proactive management, ratios climb fast.

FDCPA Compliance Complexity

The Fair Debt Collection Practices Act creates billing constraints and documentation requirements that standard processors are not equipped to evaluate.

Blanket Category Rejections

Most national banks decline debt collection accounts by policy, regardless of licensing, compliance posture, or volume.

Multi-Channel Payment Collection

Effective debt recovery requires accepting credit cards, debit cards, and ACH payments. Many specialty processors only offer one or two of these methods.

Built for Debt Collection

FDCPA-Aware Underwriting

Our underwriting team evaluates collection agencies on compliance posture and licensing, not category alone.

Chargeback Alert Integration

Ethoca and Verifi alerts catch incoming disputes before they post, protecting recovery revenue.

ACH Processing

Accept ACH payments alongside credit and debit cards to maximize recovery options across your debtor portfolio.

Secure Payment Portal

Offer debtors a secure self-service payment portal to increase voluntary payment rates.

High-Volume Processing

Underwriting built for the transaction volumes common in large collection portfolios.

Dedicated Account Manager

A named account manager experienced with collection agency payment risk, available around the clock.

Corepay By the Numbers

-

24-72h Typical Approval Window

-

98% Uptime SLA

-

135+ Currencies Supported

Processing Payments in 30+ Countries

United States

50 statesFull domestic processing with next-day funding and dedicated account management.

European Union

27 member statesPSD2 and SCA compliant processing across all EU member states with multi-currency settlement.

United Kingdom

England, Scotland, Wales, NIFCA-regulated payment processing with GBP settlement and local acquiring.

Australia

All territoriesAPRA-compliant processing with AUD settlement and Asia-Pacific connectivity.

Collection agencies need reliable payment processing with no surprises. Whether you collect payments over the internet, by phone, or through the mail, having the right merchant account is critical to your cash flow. By adding electronic payment processing, you automate collections and make it easier for debtors to pay through recurring billing plans.

We provide processing for loan service providers, student loan collection, subscription debt collection, healthcare debt consolidation, payday loan collection, personal debt collection, installment lending, auto lender collection, and agencies that buy debt.

Applying for Your Account

We aim to approve accounts within 24 to 72 hours. We waive all application, setup, and annual fees. You will need:

- Proof of business bank account

- Compliant website

- Payment processing history

- Business and personal financial history

- Photo I.D.

- Age of the business

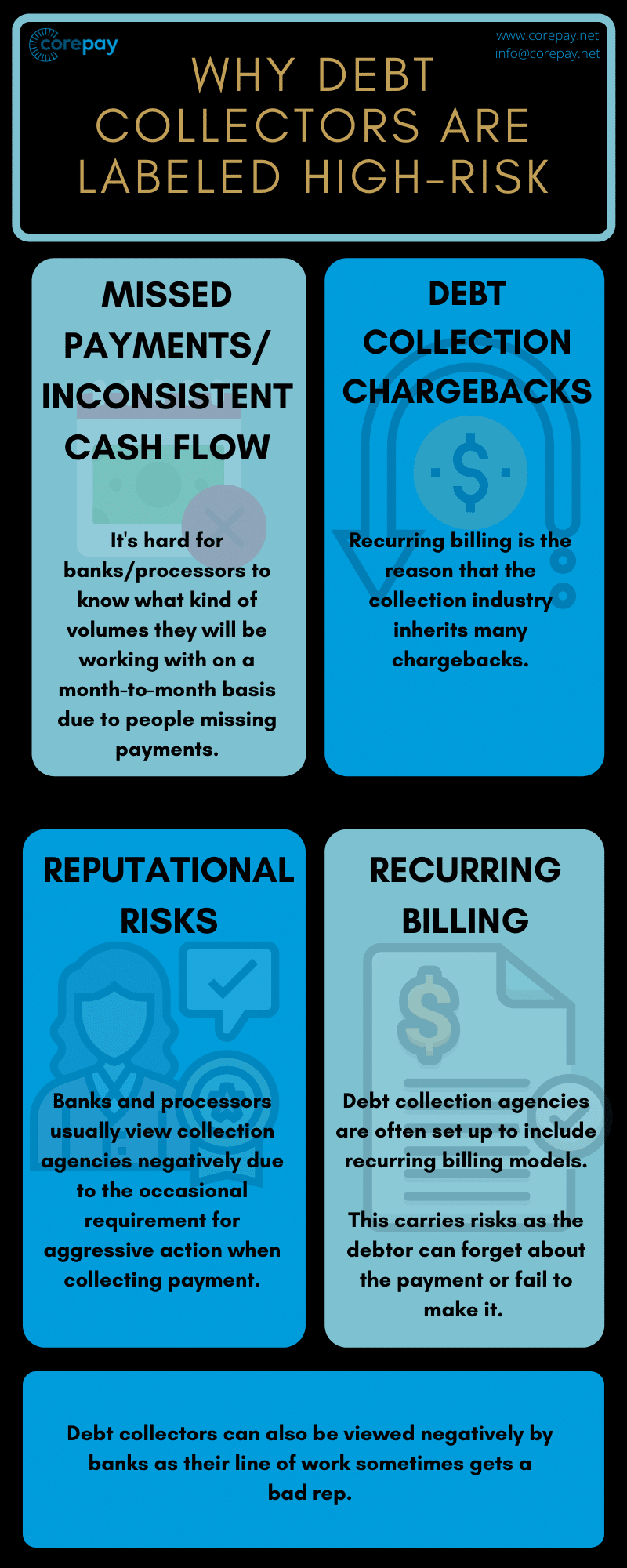

Why Debt Collectors Are High-Risk

Debt collection agencies face several risk factors. Missed payments create inconsistent cash flow, making it hard for banks to predict volume. Chargebacks are common, especially with recurring billing, because debtors may set up automatic payments and then dispute them. Reputational risk is also a factor, since collection work can carry negative perceptions. And recurring billing models inherently add risk when debtors cannot sustain the payment schedule.

ACH Over Credit Cards

ACH payments take funds directly from a debtor’s bank account. This is often better for debt collection than credit cards, because bank accounts change less frequently than card numbers and ACH exposes your business to less chargeback risk. It is also more cost-effective for collecting recurring payments.

Multiple Payment Methods

Having the ability to accept different forms of payment increases overall cash flow. The primary electronic methods debtors use are debit cards, credit cards, and ACH. While credit cards are convenient, debit cards and ACH offer significant advantages for the collection model.

Choosing the Right Processor

When selecting a merchant account provider, the most important factor is making sure they specialize in high-risk businesses. Look for transparent pricing, since some processors present convoluted statements loaded with hidden fees. Compare rates across providers. And make sure the processor offers 24/7 customer service and chargeback management tools.

Why Choose Corepay

- Approvals within 24 to 72 hours

- Waived application, setup, and annual fees

- Risk mitigation through Order Insight

- Rates as low as a blended 2.95%

- Recurring billing support

- Mobile payment acceptance

- 24/7 customer service